.jpeg)

Table of Contents

Key takeaways

- Companies with mature AI capabilities grow revenue 18.1% year over year versus 6.2% for earliest-stage organizations, a gap of nearly 12 percentage points.

- AI leaders deploy broader, higher-value use cases, with maturity gaps of 29 points in revenue and spend data classification, 24 in auto-generated summaries, and 16 in scenario planning.

- High costs, data quality, and compliance concerns remain common barriers, while lack of internal expertise and unclear ROI decline steadily as AI maturity rises.

- AI returns compound late in the maturity curve, with decision-making quality rising from 50% in advanced organizations to 69% in leading ones.

- The biggest performance jump appears when companies move from pilots to scaled, embedded AI, yet only 64% of surveyed companies have crossed that threshold.

- Leading firms plan 30% AI budget increases versus 7.8% for early-stage organizations, while 79% of respondents report higher AI usage last quarter.

New data from the Pigment Uncertainty Index shows that companies that identified their AI capabilities as "mature" in Pigment’s Uncertainty Index grew their revenue by 18.1% year over year, compared to 6.2% for organizations at the earliest maturity stage – a gap of nearly 12 percentage points.

The data is also consistent with independent research. BCG's analysis of what it calls "future-built" companies – or companies that have embedded AI across the enterprise – shows 1.7x revenue growth of their slower-moving peers, 3.6x the three-year total shareholder return, and 1.6x the EBIT margin.

And PwC found that three-quarters of AI’s economic gains are being captured by 20% of companies.

So what are these companies doing differently?

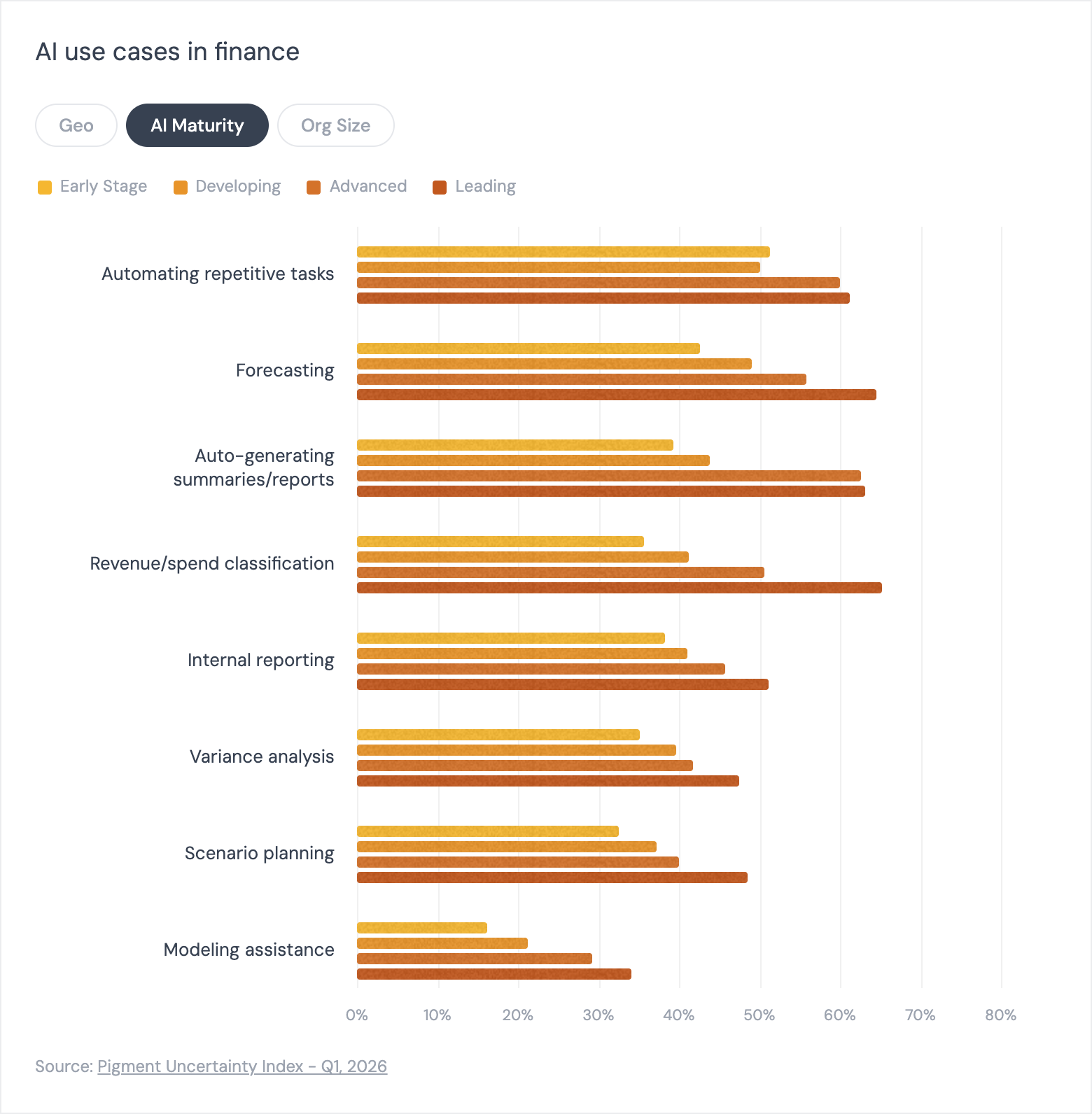

They’re deploying AI across broader and more valuable use cases

The first and most obvious trend that jumps out of the data is that the use cases that separate leaders from early-stage adopters are the ones that require AI to do real analytical work.

The gap between early-stage and leading firms in revenue and spend data classification is 29 percentage points. In auto-generating summaries and reports, it's 24 points. In scenario planning, it's 16. The areas where the gap is smallest are the ones that involve the least cognitive lift, like automating repetitive tasks.

They’re also more likely to make use of AI for more ‘entry level’ use cases like automating repetitive tasks and internal reporting, but the adoption rate between maturity levels is less pronounced here.

But how are leaders able to deploy AI across these more complex use cases?

They’re overcoming barriers

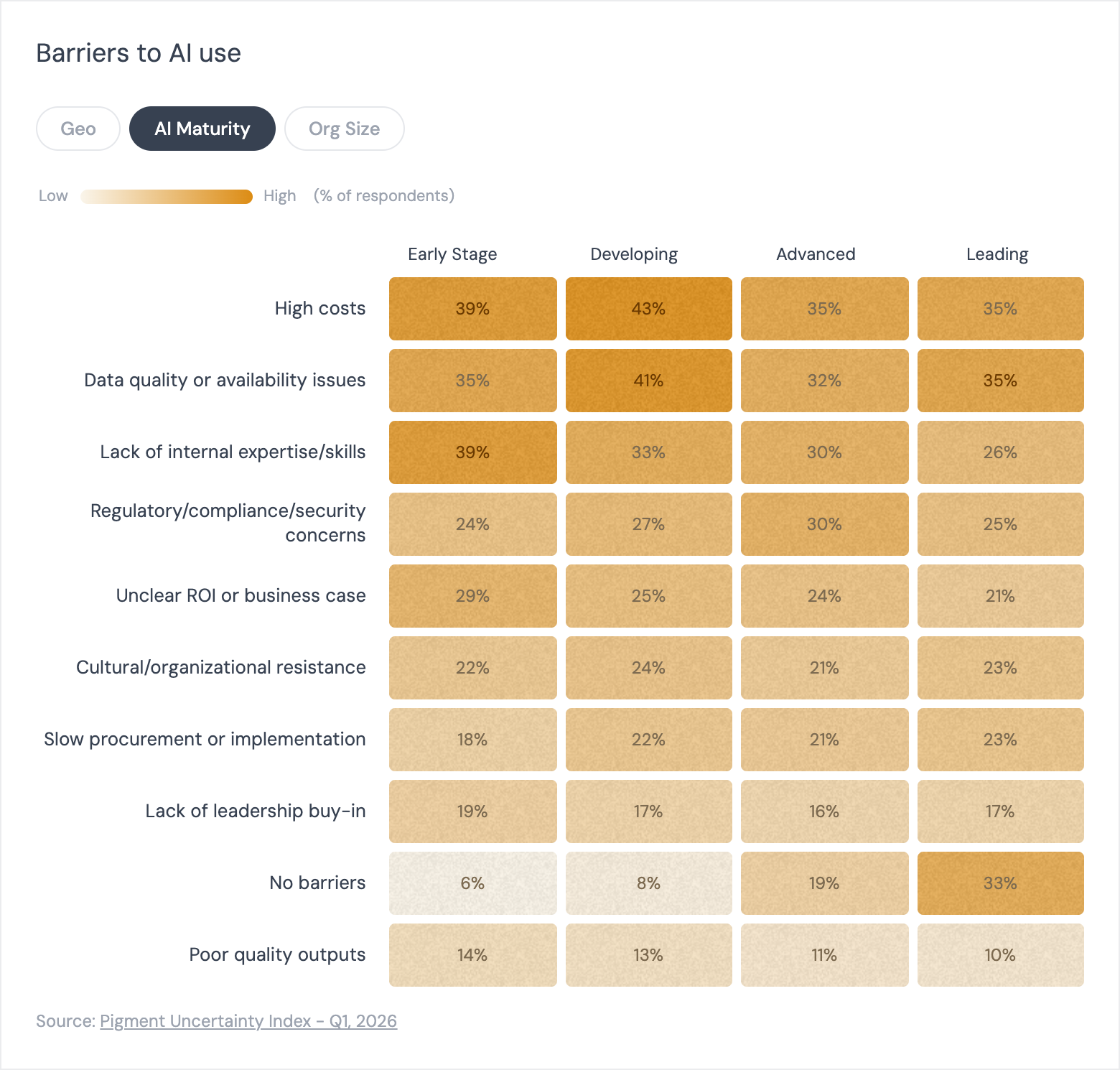

If we look at the data on what respondents felt was holding them back, we can identify some interesting nuggets.

Some issues remain broadly consistent across maturity levels - high costs, data quality/availability, and regulatory/compliance/security concerns, for example.

We can see that ‘lack of internal expertise’ and ‘unclear ROI or business case’ show a clear downward trend as you move up the maturity levels. There are two lessons to learn here:

- AI expertise is a real difference maker. If you’re a leader, you should be thinking about ways to improve the AI fluency of your team, and if you’re a contributor you should be thinking about personal development. We cover both in this guide: Upskill your finance team for AI.

- Understanding specifically what you want to use AI for, and how you’re going to track if it’s working, should be a key priority. As KPMG put it: "This is not simply an AI maturity gap; it is a widening performance gap between organizations that treat AI as enterprise-wide transformation and those bolting AI onto existing models."

That’s not to say the other barriers shouldn’t be a concern - but the data would suggest that tackling those two will net you consistent returns.

The ROI from AI investment is non-linear, and it compounds

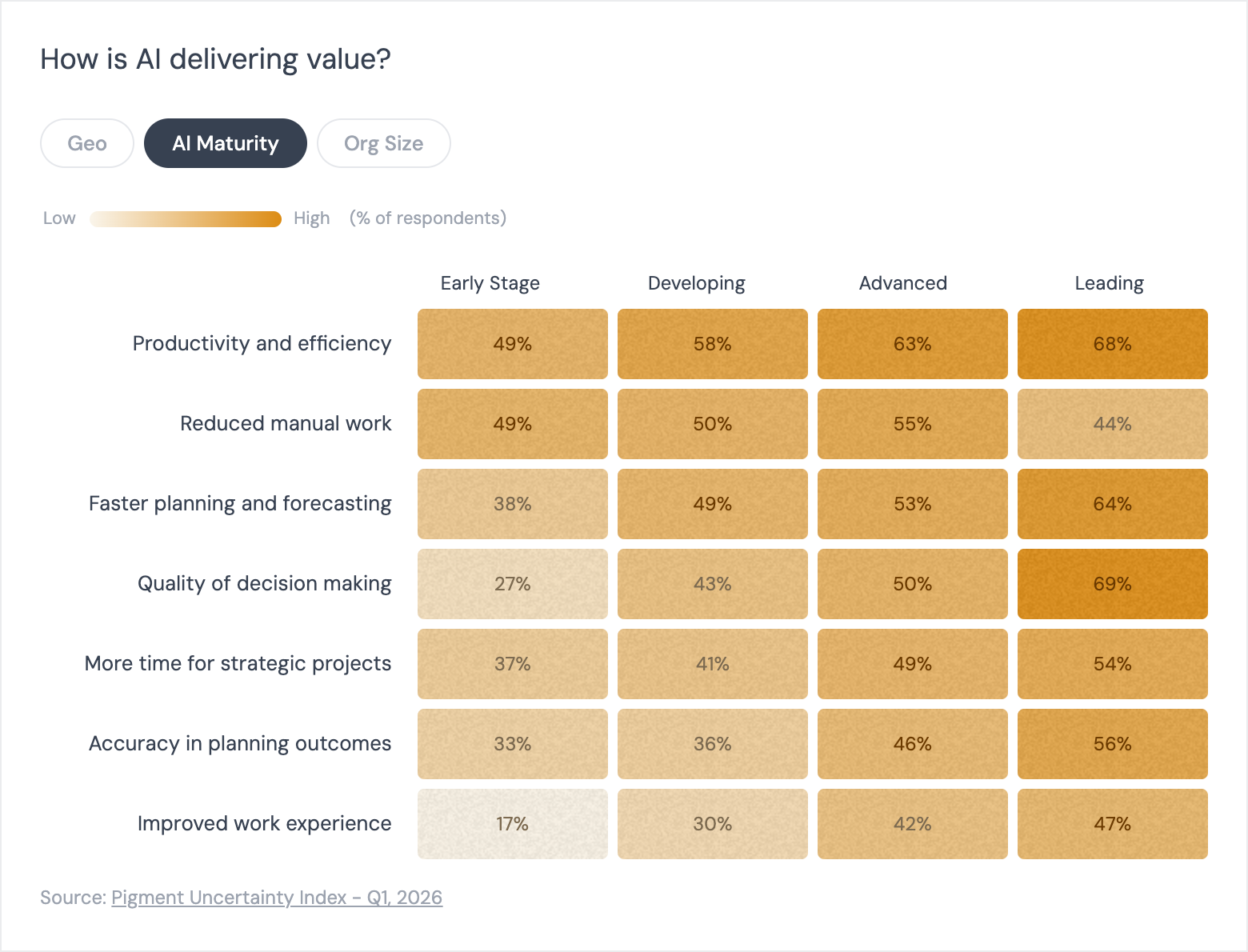

Another trend to bear in mind is that AI returns don't accumulate evenly in the data we have on perceived benefits.

Quality of decision-making is cited by 50% of advanced organizations and 69% of leading ones – a 19-point jump that doesn't materialize until late in the maturity curve. Accuracy and confidence in planning outcomes rises from 35% at the developing stage to 56% at the leading stage. Faster planning cycles show an 11-point increase between advanced and leading firms.

These aren't incremental productivity improvements; the data represents the transformation of what finance teams are capable of doing.

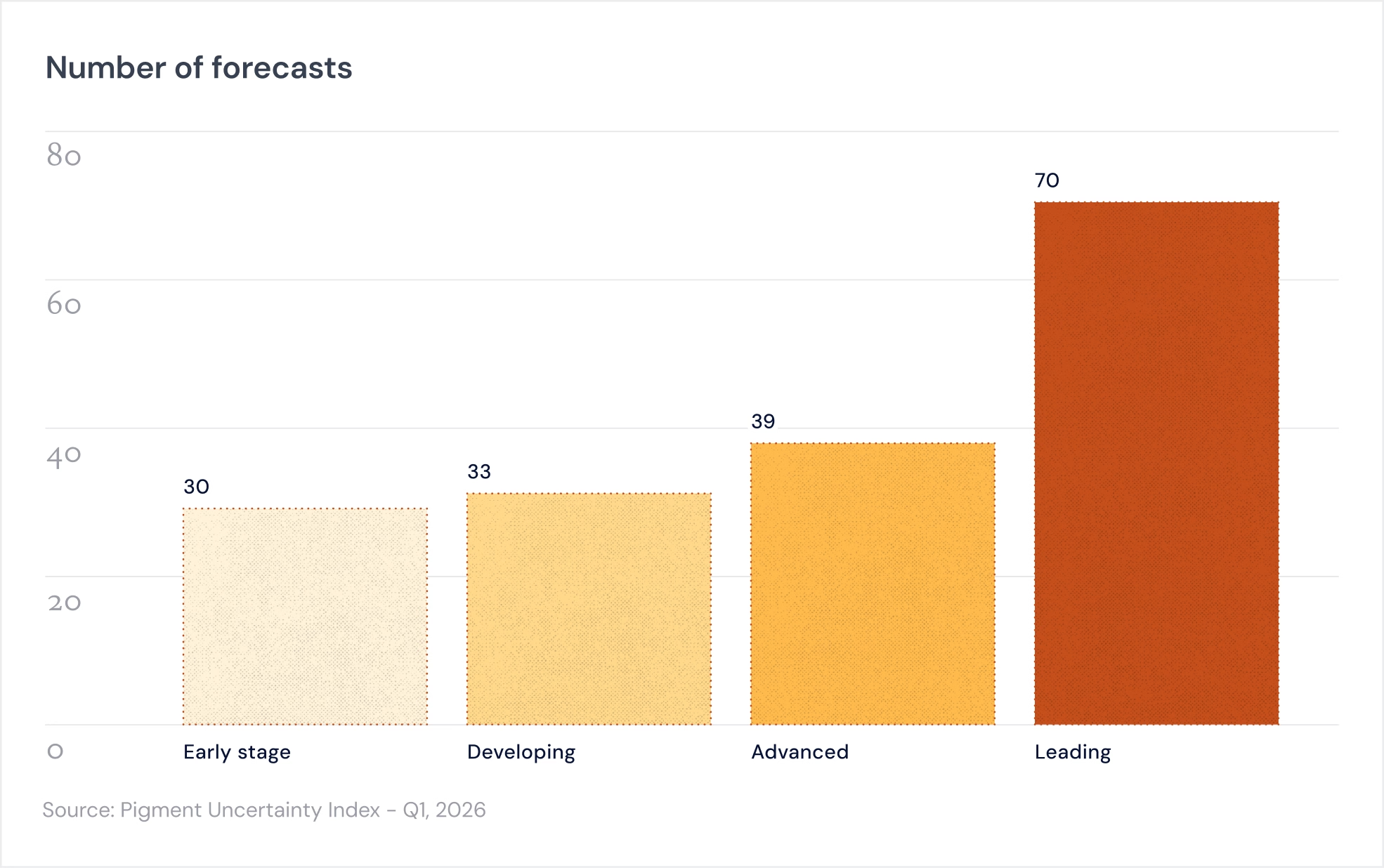

And this trend shows up when we look at data on forecasting cycles run. Firms leading on AI are showing a dramatically higher capacity to produce forecasts:

This pattern aligns with what MIT CISR found when they mapped enterprise AI maturity to financial performance across four stages. Firms in the first two stages (piloting and building capabilities) had financial performance below their industry average. Firms in stages three and four (scaling AI and becoming what they call "AI future-ready") were well above average.

The biggest jump in financial performance came at the transition between stages two and three, or the moment when pilots give way to scaled, embedded AI practices. As of 2025, only 64% of companies surveyed had crossed that threshold. The same dynamic shows up in our data in the jump from advanced to leading.

Deloitte's 2025 survey of 1,854 executives found that most organizations achieve satisfactory AI ROI within two to four years – three to four times longer than the payback period typically expected for technology investments, with only 6% seeing returns within a year. Organizations that treat AI as a series of short-term experiments, and measure success by early returns alone, are unlikely to make it to the part of the curve where the investment pays off.

All this is driving a gap in investment.

Leading firms are investing at nearly four times the rate of early-stage organizations

Our survey found that 79% of respondents increased their AI usage last quarter, and the average planned budget increase for the year ahead is 17%. But that average obscures the real story. Leading AI firms are planning a 30% budget increase. Early-stage organizations are planning 7.8%.

That 22-point gap shows the role direct evidence plays in investment. Organizations that have already seen the performance uplift of mature AI are investing in more of it, faster. Those that haven't seen it yet are moving more cautiously. BCG found the same pattern: future-built companies planned to spend more than twice what early-stage companies spend on AI in 2025. Only 5% of companies have reached that future-built threshold; 60% are still early-stage companies, seeing minimal gains.

What makes this particularly consequential right now is the external environment. According to our data, the biggest drivers of uncertainty are macroeconomic conditions, cost and margin pressure, and regulatory change. In 2026, every planning team must have the ability to reforecast quickly, model multiple scenarios, and absorb new information without losing planning momentum.

AI maturity also reduces the likelihood that macroeconomic conditions or cost pressure even register as barriers to AI success. It isn’t that leading firms are insulated from macro volatility, but they do have better tools to navigate it.

The Stanford AI Index notes that 88% of organizations are now using AI and that AI-driven enterprise revenues are growing faster than any prior tech boom. Despite this, most of the value remains concentrated at the top of the maturity distribution.

Three out of four global leaders surveyed by KPMG say they will prioritize AI investment even in the face of economic uncertainty. The logic is straightforward: in volatile environments, forecasting capability, speed, and scenario coverage are more valuable than they were when the operating environment was stable. The organizations that have already built those capabilities are not going to stop investing in them.

But the gap between AI leaders and early-stage adopters doesn’t have to be permanent

The relationship between AI maturity and business outcomes in our data is significant. Leading firms are outperforming on revenue, running more forecasts with greater confidence, deploying AI in harder and more valuable use cases, and investing at rates that will widen their advantage over every coming quarter.

The race to get AI right feels daunting when you're still finding your footing. But the organizations now leading weren't born running. The path they've taken is neither proprietary nor out of reach. The advantage they enjoy was built incrementally, through sustained investment and a willingness to bring AI into harder territory. It all started with an honest assessment of where they actually stood.

Take the AI Maturity Assessment →